It’s business planning not accounting. Your projections, although they look like accounting statements, are just projections. They are always going to be off one way or another, and their purpose isn’t guessing the future exactly right, but rather setting down expectations and connecting the links between spending and revenue. Then when you do your monthly reviews, having made the original projection makes adjustments easier.

This is the fifth of five principles of business planning. Others include do only what you use; it’s a process not a plan; it’s for managing change; and it develops accountability.

Planning and accounting are two different dimensions

Accounting goes from today backwards in time in ever-increasing detail. Planning, on the other hand, goes forward into the future in ever-increasing summary and aggregation.

Understanding this difference helps you with the educated guessing involved in making projections. The reports that come out of accounting, called statements, must accurately summarize the actual transactions that happened in the past. For example, a proper and correct Profit and Loss statement in accounting is a report summarizing all the actual transactions recorded as sales, costs, and expenses for a specified period of time (month, quarter, or year).

But projections, unlike financial statements, are just educated guesses. They aren’t reports of a database of actual transactions. Where accounting reports on records in a database, for projections there is no database. We guess what the totals might be. So you don’t try to imagine all the separate transactions in your head, for the future, and then report on them. You estimate the totals. That’s not only easier, but better. It’s a better match to how the projections help you manage, and how we humans deal with numbers.

You estimate and aggregate

So you don’t try to imagine all the separate transactions in your head, for the future, and then report on them. You estimate the totals. That’s not only easier, but better. It’s a better match to how the projections help you manage, and how we humans deal with numbers.

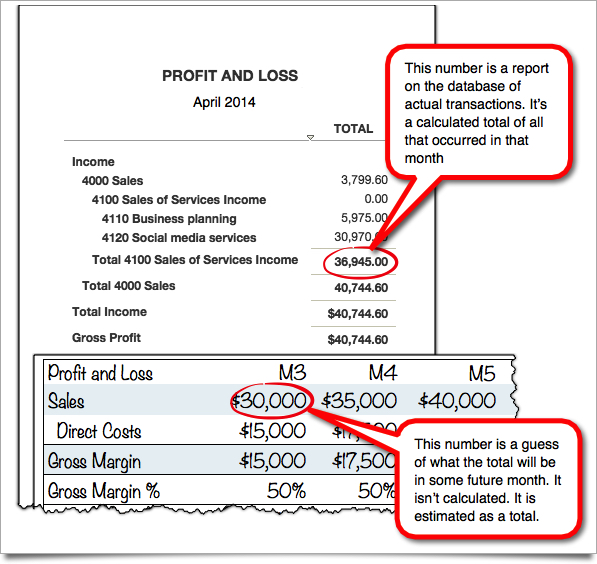

In the example below, the reported sales of $36,945.00 for services in the month of April of 2014 is a database report. Every transaction recorded in that month is included in the database. The number shown is the calculated total of all the transactions that included sales of a service item. It’s not a guess or an estimate. It’s a calculated total. On the other hand, the projected sales of $30,000 for some future month is the business owner’s guess – an educated guess, or an estimate – of what the total will be for that future month. Nobody imagines or guesses all of the individual transactions that will happen in that month in the future, and then totals them. We guess the total. The database report showing $36.950 is accounting. The projected sales of $30,000 is planning.

Comments